[ad_1]

Andrii Shablovskyi/iStock via Getty Images

A Quick Take On Mister Car Wash

Mister Car Wash, Inc. (NYSE:MCW) went public in June 2021, raising approximately $563 million in gross proceeds for the company and selling shareholders from an IPO that was priced at $15.00 per share.

The firm provides a range of car washing services throughout the United States.

MCW faces demand uncertainties, as it appears the U.S. economy is flirting with or already in a recession.

Given these macroeconomic risks and a stock that appears fully valued, I’m on Hold for MCW for the near term.

Mister Car Wash Overview

Tucson, Arizona-based MCW was founded to develop a network of retail car washing locations in the U.S.

Management is headed by Chief Executive Officer Mr. John Lai, who has been with the firm since 2002 and also serves as a director of the Southern Arizona Leadership Council.

The company’s primary offerings include:

-

Exterior washing

-

Interior detailing

-

Sales of misc. accessories

The firm acquires customers through drive-by, word of mouth and various advertising and promotion efforts.

MCW has focused on selling all-you-can-wash subscription memberships, which represented 70% of the firm’s sales in Q1 2021 from 1.4 million members.

MCW’s Market & Competition

According to a 2020 market research report by Grand View Research, the global car wash service was an estimated $33 billion in 2018 and is expected to reach $41 billion by 2025.

This represents a forecast CAGR of 3.2% from 2019 to 2025.

The main drivers for this expected growth are a growing interest by consumers on the maintenance of their vehicles and increase in discretionary spending power.

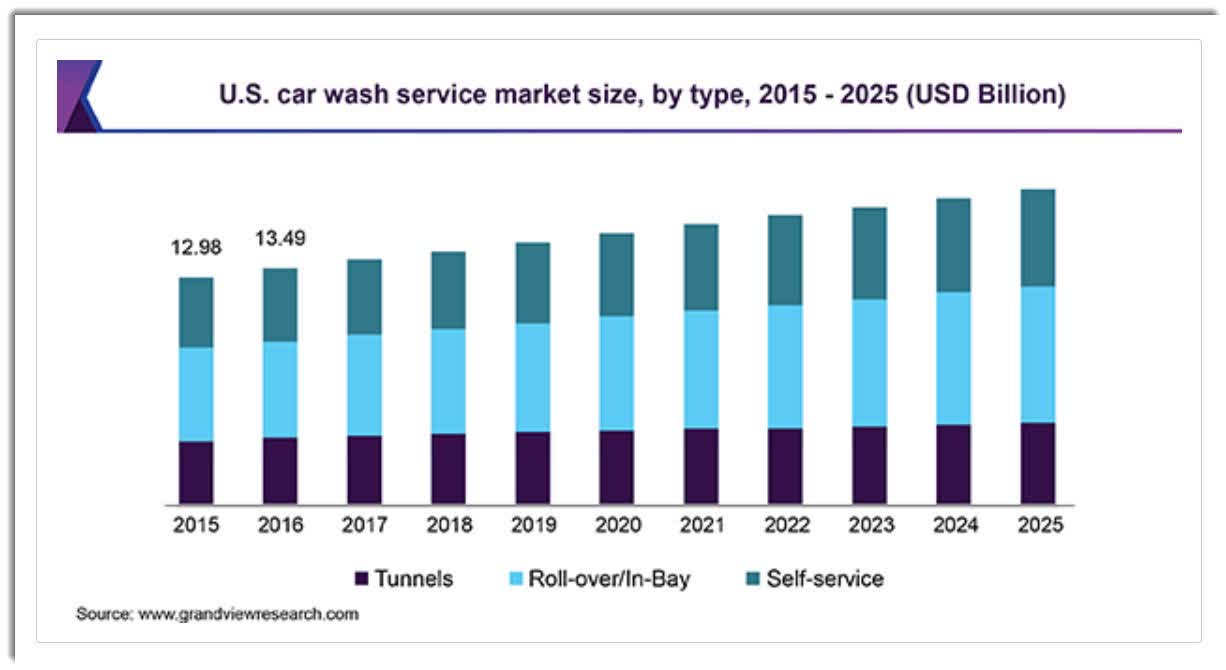

Also, below is a historical and projected future chart showing the U.S. car wash market, broken down by type of car wash:

U.S. Car Wash Market (Seeking Alpha)

Major competitive or other industry participants include:

-

Zips Car Wash

-

International Car Wash Group

-

Autobell Car Wash

-

Quick Quack Car Wash

-

Super Star Car Wash

-

True Blue Car Wash

-

Magic Hand Car Wash

-

Hoffman Car Wash

-

Wash Depot Holdings

-

Other small operators

MCW’s Recent Financial Performance

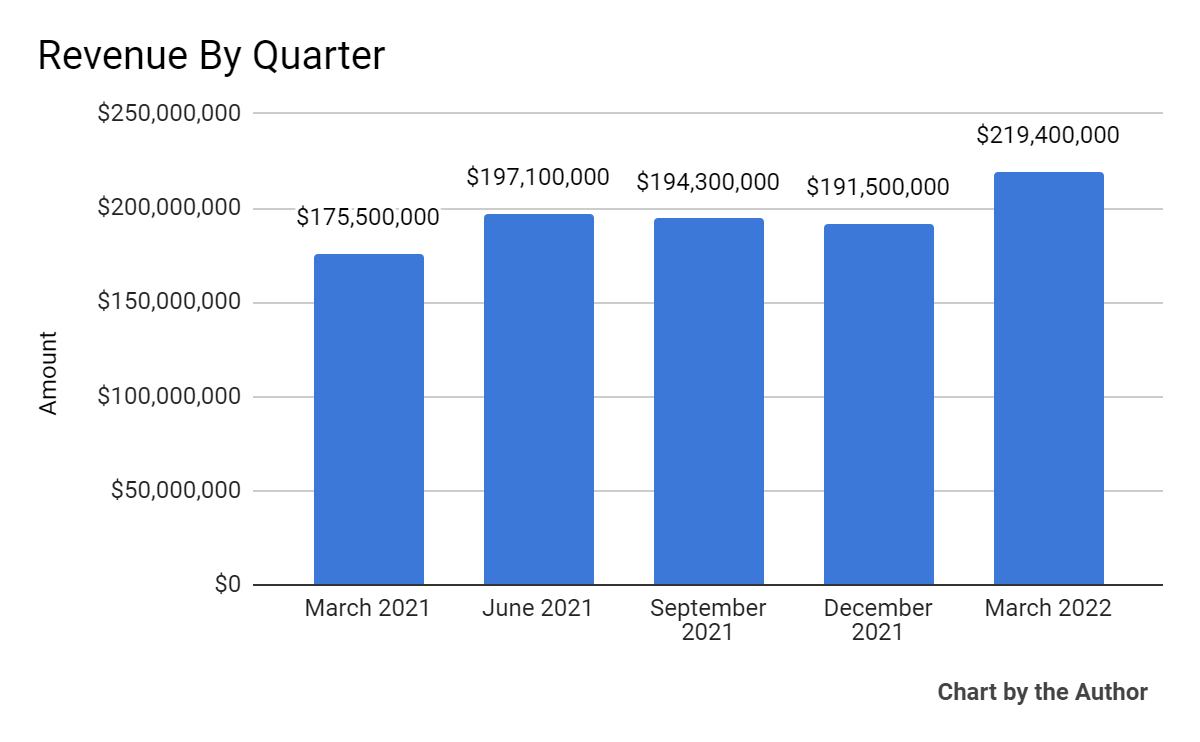

-

Total revenue by quarter has risen, although affected by seasonal factors:

5 Quarter Total Revenue (Seeking Alpha)

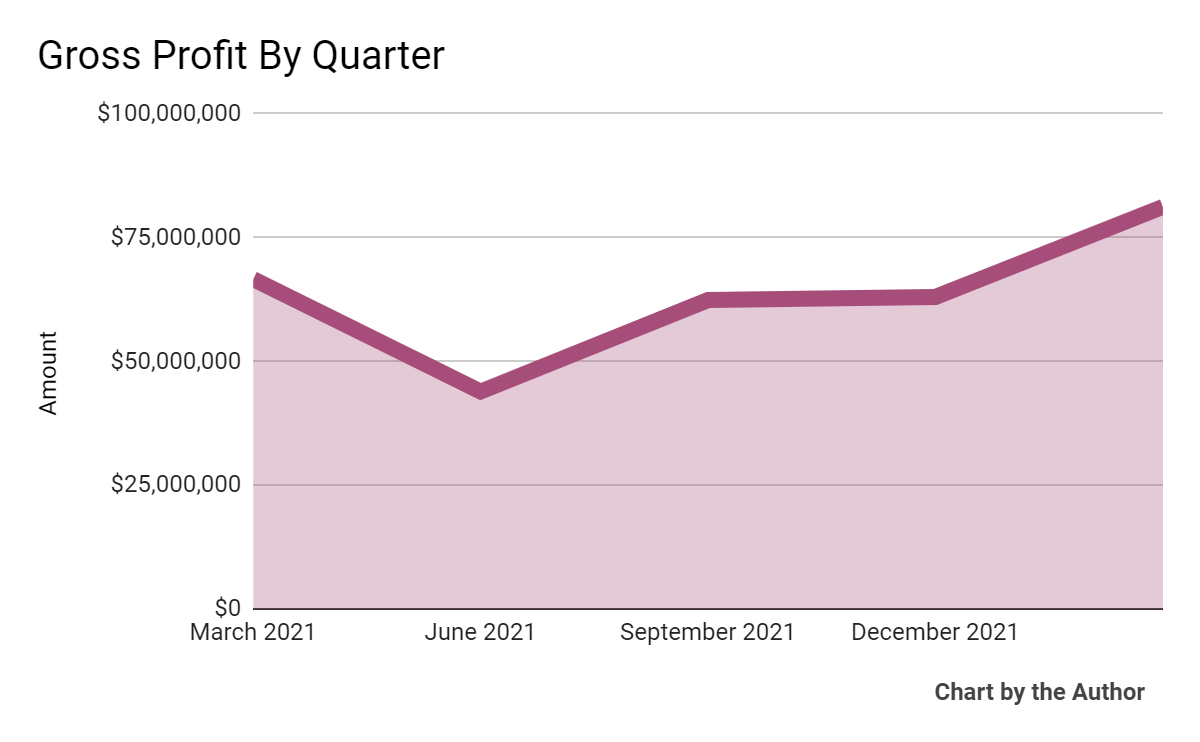

-

Gross profit by quarter has grown, but unevenly:

5 Quarter Gross Profit (Seeking Alpha)

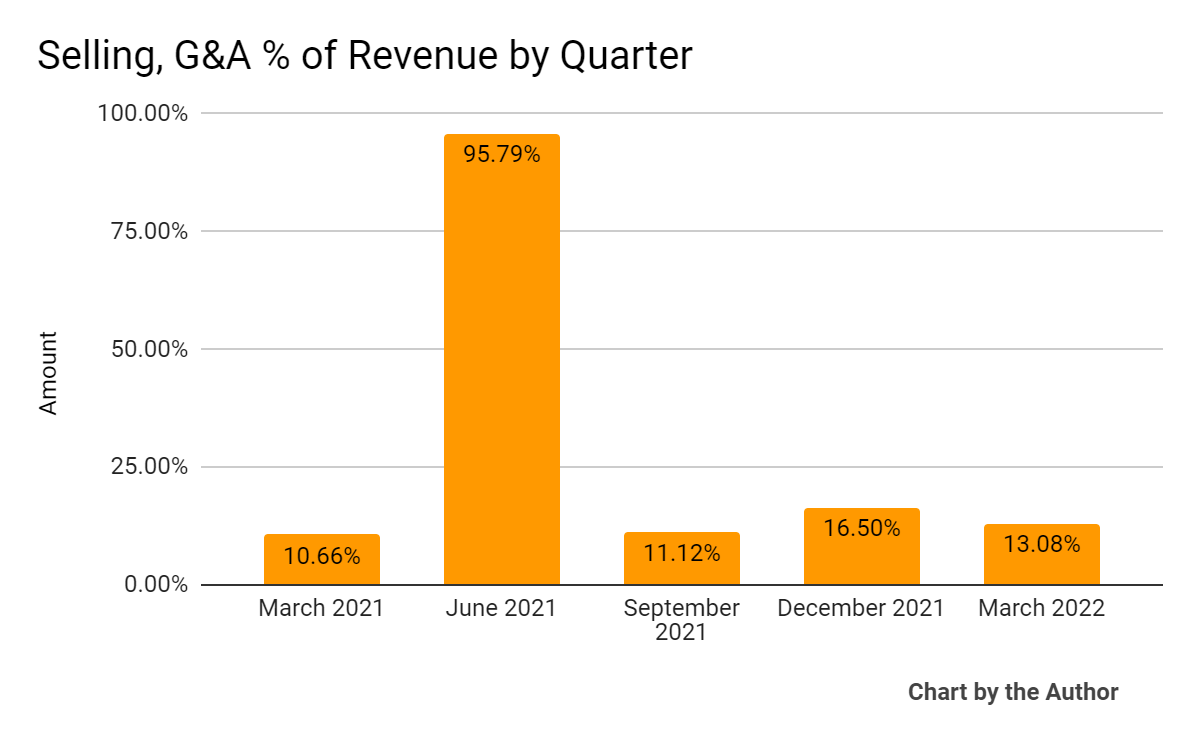

-

Selling, G&A expenses as a percentage of total revenue by quarter have remained in the low teens, with the exception of the Q2 2021 quarter which contained stock-based compensation related to the IPO:

5 Quarter Selling, G&A % Of Revenue (Seeking Alpha)

-

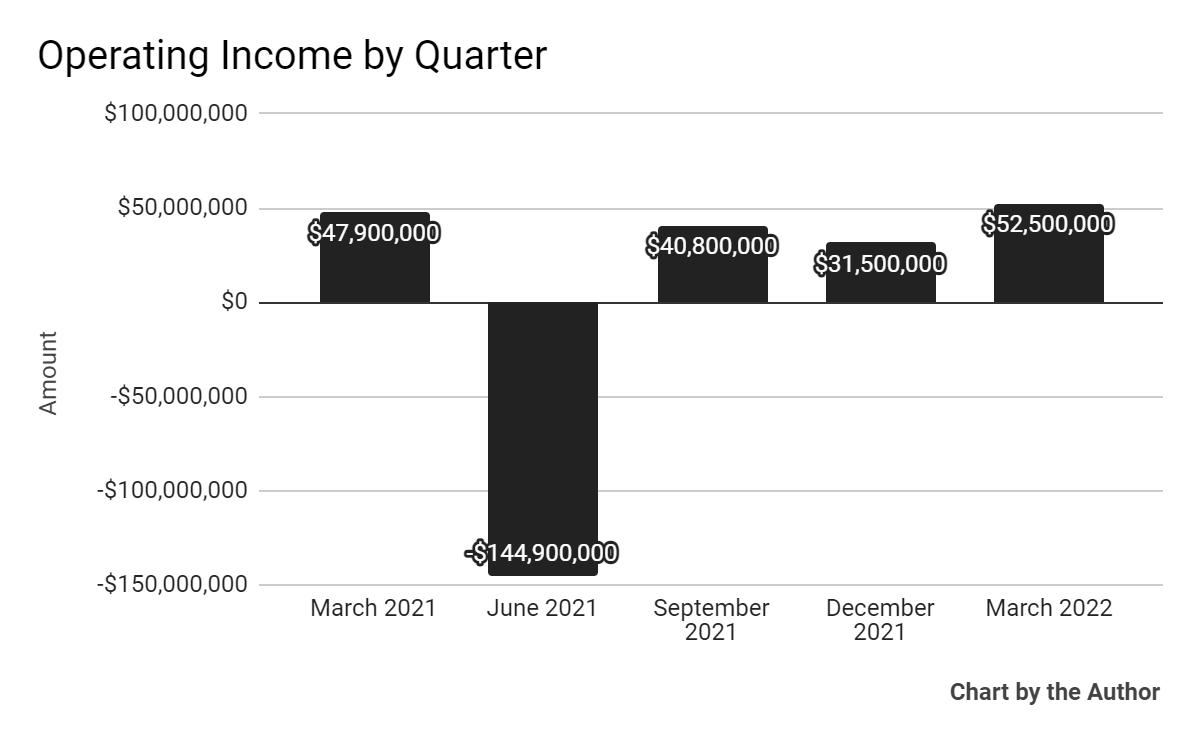

Operating income by quarter has grown in recent quarters:

5 Quarter Operating Income (Seeking Alpha)

-

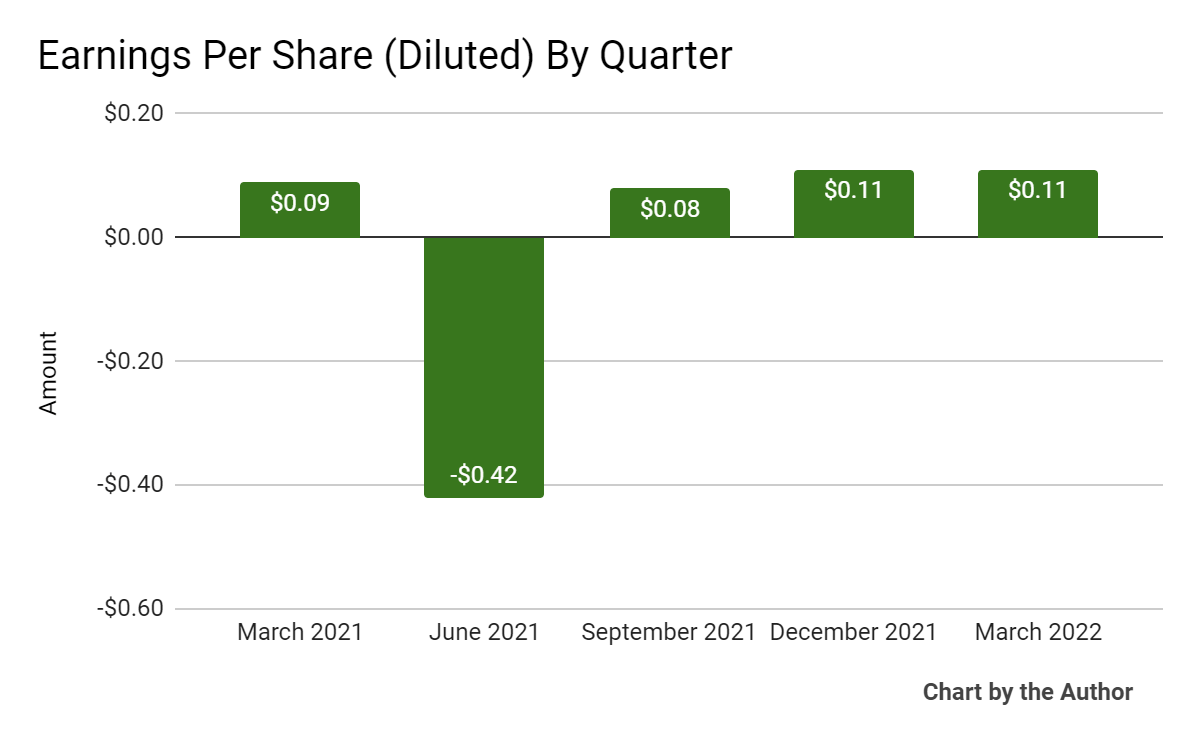

Earnings per share (Diluted) have generally followed the same trajectory as that of operating income:

5 Quarter Earnings Per Share (Seeking Alpha)

(All data in above charts is GAAP)

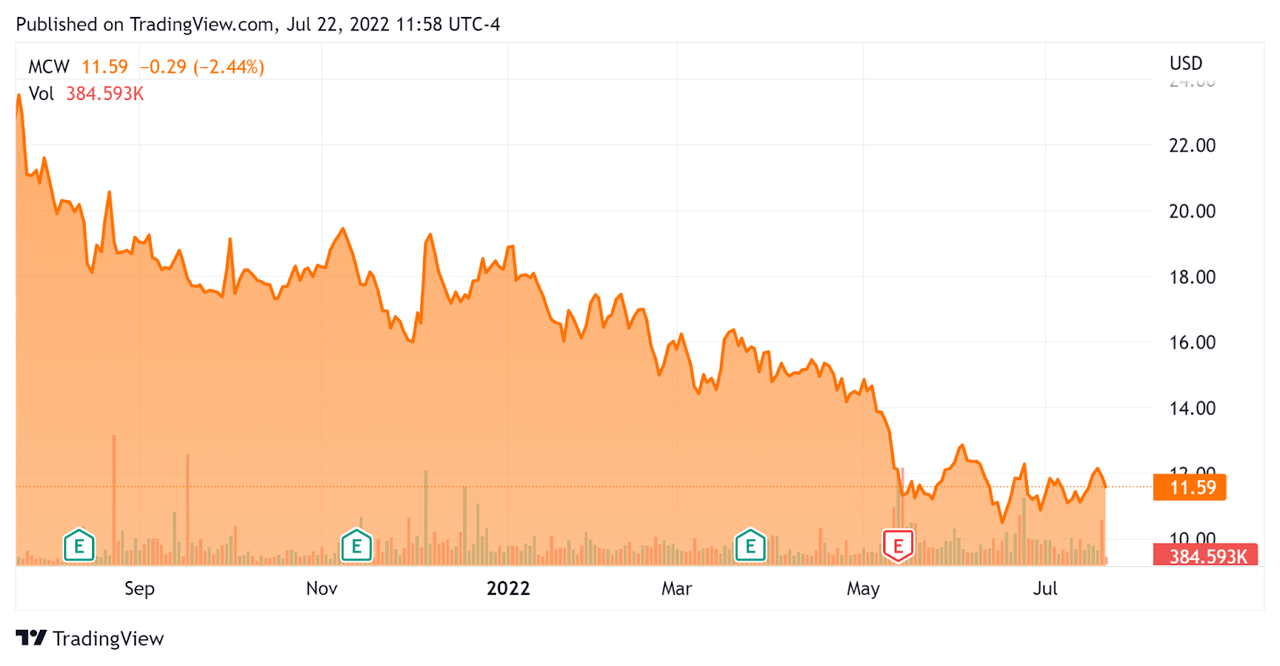

In the past 12 months, MCW’s stock price has dropped 48.8 percent vs. the U.S. S&P 500 Index’s drop of around 9.0 percent, as the chart below indicates:

52 Week Stock Price (Seeking Alpha)

Valuation And Other Metrics For MCW

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure |

Amount |

|

Enterprise Value |

$5,180,000,000 |

|

Market Capitalization |

$3,590,000,000 |

|

Enterprise Value/Sales (TTM) |

6.46 |

|

Price/Sales (TTM) |

4.29 |

|

Revenue Growth Rate (TTM) |

34.79% |

|

Operating Cash Flow (TTM) |

$203,310,000 |

|

CapEx Ratio (Op C.F./CapEx) |

1.65 |

|

Earnings Per Share (Fully Diluted) |

-$0.12 |

(Source – Seeking Alpha)

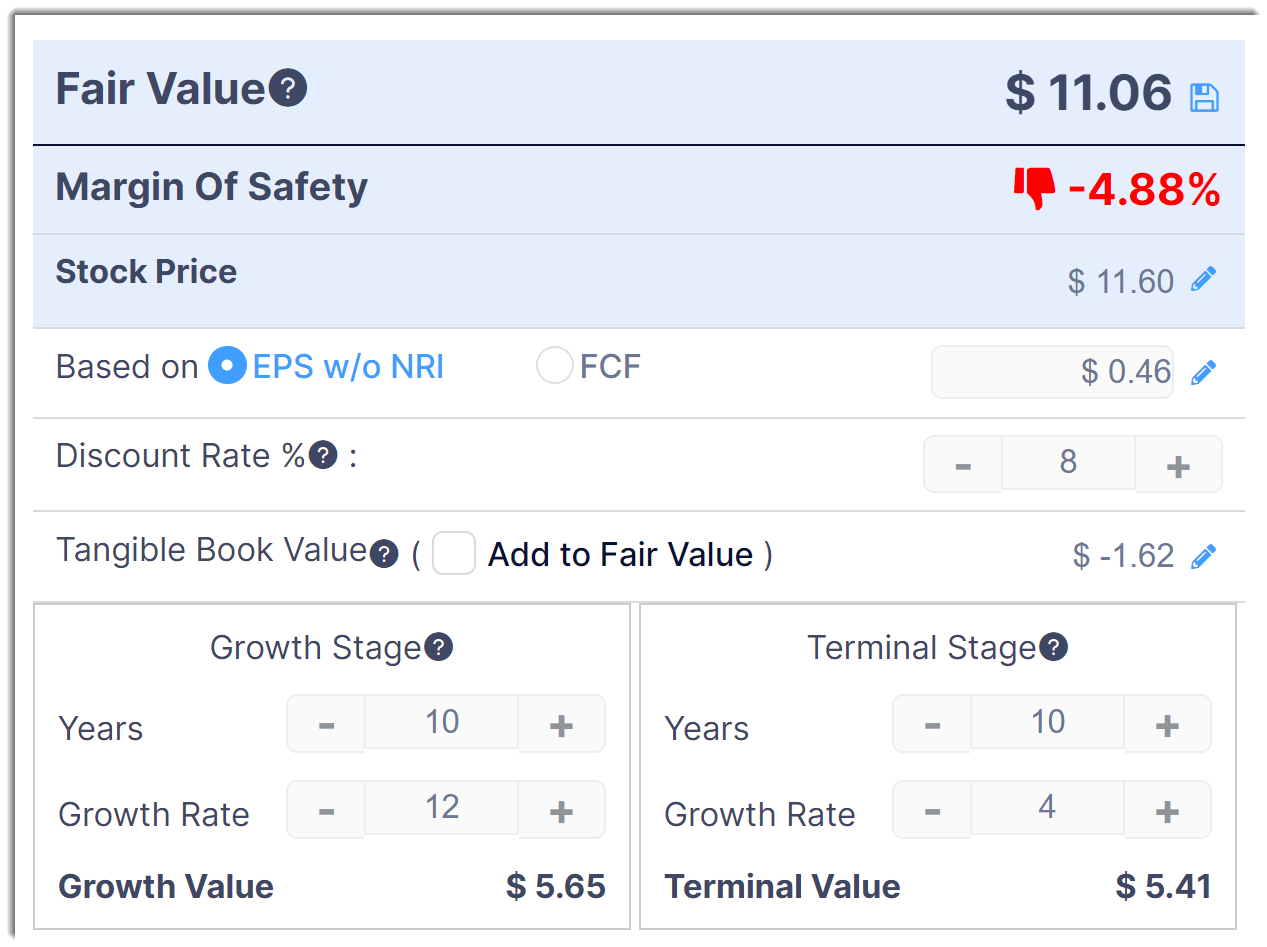

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

MCW – Discounted Cash Flow (GuruFocus)

Assuming generous DCF parameters, the firm’s shares would be valued at approximately $11.06 versus the current price of around $11.60. This indicates they are potentially currently fully valued, with the given earnings, growth, and discount rate assumptions of the DCF.

Commentary On MCW

In its last earnings call (Source – Seeking Alpha), covering Q1 2022’s results, management highlighted the addition of 125,000 new unlimited wash club members.

The company also continued to acquire assets “that complement our footprint and allow us strategic entry into a market.” To that end, MCW recently acquired four locations in the southern California high desert area of Victor Valley, which is a high-growth region.

MCW is contending with a tight labor market, but management says its stores “remain fully staffed,” despite an Omicron surge in January that led to some health-related sick day increases.

As to its financial results, total revenue grew 25% year-over-year and same-store sales growth for stores open more than a year rose by 11%.

As for expenses, MCW experienced increasing labor and chemicals costs but increased G&A costs associated with its expansion plans.

For the balance sheet, the firm finished the quarter with cash and equivalents of $70 million and positive free cash flow for the quarter of $51.5 million. Long-term debt was $895 million.

Looking ahead, management reiterated its full-year guidance, with revenue expected to be $885 million at the midpoint of the range and GAAP net income of $144 million or around $0.46 per diluted share.

Regarding valuation, a DCF with generous long-term growth rate assumptions indicates the company’s shares are fully valued are its current growth and earnings.

The primary risk to the company’s outlook would be a U.S. recession, which would reduce customer demand for some of its more discretionary services.

A potential upside catalyst to the stock could include a reduction in interest rate expectations, which may have the effect of increasing its valuation multiple.

However, the firm faces uncertainties as it appears the U.S. economy is flirting with or already in a recession.

Given these macroeconomic risks and a stock that appears fully valued, I’m on Hold for MCW for the near term.

[ad_2]

Source link

More Stories

Ebook Review – Auto Auction Income

Glass Industry Terms – Everything You’ve Always Wanted to Know About Glass But Were Afraid to Ask

The Importance of Technical Knowledge in Modern Auto Sales Training